The board has approved the Fund's financial statements for the year 2025.

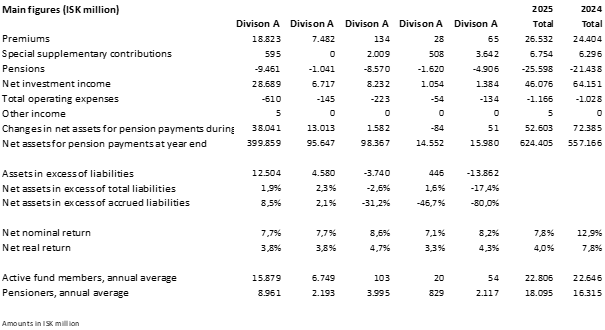

The Fund's net assets for pension payments at year-end 2025 amounted to ISK 624.405 million but was ISK 557.166 million at year-end 2024 and increased by ISK 67.239 million between years. Of this amount, net assets of the pension fund; Lífeyrissjóður starfsmanna Akureyrarbæjar (LSA), at the beginning of the year were ISK 14.636 million, but LSA was merged with Brú in a new E division at the beginning of 2025. The net nominal return of Brú was 7.8% and net real return was 4.0%.

Fund members and premiums

Premiums amounted to ISK 33.286 million in 2025 (2024: ISK 30.700 million), thereof ISK 6.754 million were due to additional contributions. An average of 22,806 individuals paid contributions to the fund (2024: 22,646) and are divided between divisions as follows:

Pensioners and pension payments

The Fund paid ISK 25.598 million in pensions in 2025 (2024: ISK 21.438 million), of which ISK 20.032 million was in retirement pensions and ISK 3.202 million in disability pension. On average, 18,095 individuals received pension from Brú in 2025 (2024: 16,315) and they were divided between divisions as follows:

Actuarial review

Actuarial review is done especially for each division of the Fund and underlying portfolios. The calculation for A and V division is based on that annual real interest rate of assets will be 3,5% in the coming years and for R, E and B divisions it is assumed that the real return will be 2,0% annually in excess of the increase in pension rights.

Total assets in excess of total liabilities divides between divisions as follows:

The ratio of total assets to total liabilities of each division is as follows:

The result of the actuarial examination for A and V division are within the limits required in Article 39. Act no. 129/1997 on the mandatory insurance of pension rights and the operation of pension funds.

The calculation assumptions for disability, marriage and child probabilities are unchanged from the Fund's last actuarial review. Disability probabilities are based on experience of the years 2018-2023 and are then adjusted to the experience of each division of the Fund. The probability of marriage and childbearing is based on the experience of the years 2019-2023.

Return on investment

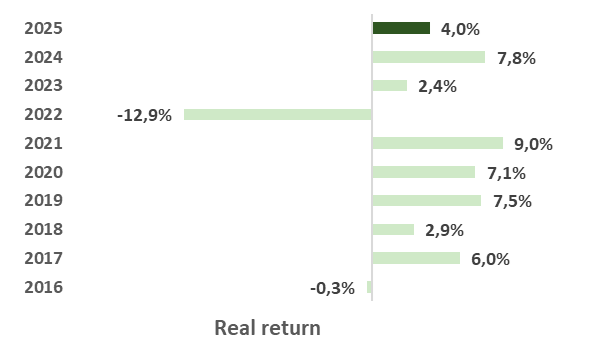

The Fund's real return was 4.0% in 2025 (2024: +7.8%) and the nominal return was 7.8% (2023: +12.9%). The pension fund is a long-term investor and has delivered good returns in recent years, with the exception of 2022. Average net real return over the past 5 years was 1.7% and for the past 10 years 3.1%, which is slightly below the benchmark set by pension funds, but pension funds are expected to achieve an average real return of 3.5% per year.

The year's return is acceptable compared to previous years, but the year was characterized by significant market fluctuations and increased tension in the global economy. The return on domestic equities exceeded the index, and returns remained good in foreign equity markets. Inflation, however, was persistent, and interest rates remained high. During the year, settlements were carried out on bonds issued by the Housing Finance Fund (HFF bonds), and the state delivered a portfolio of government bonds along with cash for their settlement. The domestic equity index fell by 7.45% during the year compared to an increase of 12.62% in 2024, but there was an increase in the domestic bond market.

Green Assets

The Fund provides information on the proportion of the Fund's assets that are considered green assets in accordance with the EU Taxonomy Regulation (2020/852). This regulation defines how sustainable or green a company's economic activity is considered to be, but companies in the financial market must use the information to inform how it is reflected in their operations.

The green ownership ratio of individual divisions was between 0,4% and 2,9% at year-end. It is calculatedbased on the turnover or investment fees of the underlying companies and includes all investment assets of the Fund, excluding assets with a government guarantee.

One of the goals of the EU classification regulation is to promote investment in sustainable operations and prevent greenwashing. The regulation entered into force on June 1, 2023, but the EEA sustainability framework has recently been revised with the aim of reducing the information burden for companies and simplifying the implementation of the regulation. It is clear that the arrangement and scope of this disclosure will undergo changes in the coming years. Information published here should therefore be viewed with caution, as the implementation and development of sustainability information is still in its early stages.

The main figures of the year are shown in the table below: